Liz Sonders je rekla da je kraj recesije (u USA) bio u julu-avgustu. Mislim da je tu bila u pravu, oficijelni stav NBER-a chemo saznati tek nekad slijedece godine. Takodjer je 2007-me bila 'zabrinuta' za realestate/financial bubble.

To su joj mogle i biti koincidencije, a za ovo dole chu je pratiti da vidim jeli bila upravu...

Inflation bogeyman not as scary as he looks

http://www.schwab.com/public/schwab/res ... ition=T005

Schwab's Liz Ann Sonders analysis...

...

There's a growing concern about a major inflationary threat posed by our burgeoning deficit, very easy monetary accommodation, and the weakening dollar—further highlighted by the sharp rally in the price of gold.

We remain in the camp that there's no imminent price inflation risk on the horizon, largely thanks to the pressure that remains on wages and unit labor costs (due to weak labor demand), a historically low capacity utilization rate, diminutive lending by financial institutions, and benign market-based indications of inflation risk. Treasury Inflation-Protected Securities (TIPS) are telling us inflation will be under 2% for the next 10 years.

Many folks with whom I've spoken assume that the budding economic recovery is also inherently inflationary. This is not the case , as the chart below shows. Historically, inflation tends to fall for a full year after recessions have ended.

Inflation generally falls as economy recovers

Click to enlarge

Core CPI is based on year-over-year percent change. Source: FactSet and the US Department of Labor as of October 19, 2009.

Another sign that inflation risk is low, presently, is the velocity of money argument—one we've used a lot to express our views.

Indeed, money creation has surged during the past year, but there are no signs of inflation … meaning a lot of this excess money is going to shore up banks' capital bases and/or fuel asset price inflation (gold, stocks, etc.).

Velocity of money is also referred to as the money multiplier, which I explained in detail in an earlier report this year on inflation vs. deflation. Mathematically, the money multiplier equals M2 money supply divided by the monetary base. Generically, it's the amount of money getting from the banking system into the economy.

Until the velocity of money begins to accelerate, inflation is unlikely.

Monetary base up dramatically, but velocity of money remains impaired

Click to enlarge

Source: FactSet and the Federal Reserve as of October 9, 2009.

We can keep putting gas in the tank, but if there's a leak in the bottom, it won't help the car run. Our bottom line remains that inflation is not a near-term risk, although it remains a longer-term concern if deficits aren't reined in.

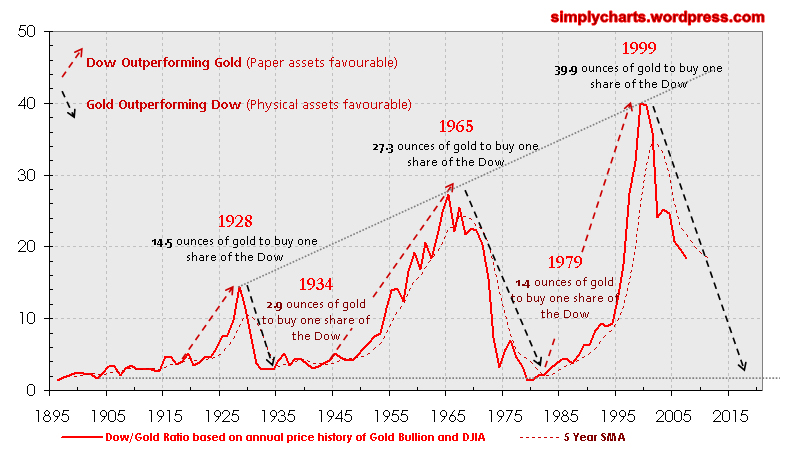

But what about gold's dramatic ascent?

Finally, many are pointing to gold trading at more than $1,057 an ounce as a harbinger of inflation.

Gold bulls abound! (Where were they all four years ago when gold was half its current price?) In contrast to conventional wisdom, gold is a dubious indicator of inflation. Historically, gold prices have risen in both inflationary and deflationary periods as highlighted in a recent report by BCA Research.

The first gold bull market was in the mid-1930s, when gold was revalued upward by 70%. This was a highly deflationary period.

The second gold bull market started in 1971, when the dollar was de-pegged to gold, causing gold prices to soar. This was an inflationary period.

The third gold bull market started in 2001 and has so far lasted for nine years. During this period, the world economy has been confronted with periodic deflation threats, first with the tech bubble bust and more recently with the financial crisis and attending recession.

The only factor that can consistently explain gold price moves is the speed of fiat money creation. Dollar-based liquidity, a measure of global money creation, has had a strong influence on the direction of gold prices since the 1980s. As BCA notes, if money creation cannot lift general inflation, excess money must find its way to asset markets, lifting asset prices. Bingo.

Recently, gold has represented a proxy for risk. If you're jumping on the gold bandwagon, be mindful of the possibility that gold could turn negative once (if?) the world economy has rebounded strongly and central banks are ready to tighten monetary policy...